Most Canadians shopping for retirement planning software start with the wrong question. They ask, "Which one is the best?" But the better question is, "Best at what, for whom, and against what criteria?"

Canadian retirement planning software is a class of tools that models a Canadian household's full retirement horizon, including RRSPs, TFSAs, FHSAs, LIRAs, CPP, OAS, real estate, and corporate accounts, to project income, tax, and net-worth outcomes across decades. The good ones don't just project. They optimize. They answer questions like when to draw from each account, how much to convert each year, and at what age to start CPP and OAS, all while minimizing lifetime tax.

This guide is criteria-led. We'll cover what you should actually look for, the real alternatives in the Canadian market, what it should cost over 10 years, and the questions most Canadians never think to ask before they pay.

What you should actually look for in Canadian retirement planning software

There are eight criteria that separate a serious retirement planning tool from a glorified retirement calculator. If a product can't tick most of these, it isn't really planning your retirement. It's drawing a line on a chart.

1. Canadian-rule accuracy

This is the floor, not the ceiling. The software must correctly model CPP (Canada Pension Plan), OAS (Old Age Security), RRSP and RRIF mechanics, FHSA (First Home Savings Account), TFSA (Tax-Free Savings Account), the OAS recovery tax (clawback), GIS (Guaranteed Income Supplement) thresholds, pension income splitting at 65, LIRA and LIF rules by province, spousal RRSP attribution, capital gains inclusion, and the principal residence exemption. If any of these are missing, the optimization isn't actually Canadian. It's American math with a maple leaf on the homepage.

2. Whole-household modelling

You don't retire alone. Real plans need to model your spouse's accounts, joint property, real estate, and, if you own a Canadian-controlled private corporation, your CCPC structure too. Pension splitting, survivor benefits, and combined OAS clawback exposure only show up properly when both partners live inside the same plan. If you're a couple, you also need spousal RRSP attribution rules handled correctly, because they can quietly wreck a withdrawal plan if you miss them.

3. True optimization vs rule-of-thumb

Most online "retirement calculators" simulate a single rule of thumb. Withdraw RRSPs first. Defer CPP to 70. Take 4% per year. Real optimization is different. It solves your deposits and your withdrawals together, every year, across every account, weighing your marginal tax bracket, your OAS clawback exposure, and pension splitting opportunities all at once. A proper engine will surface strategies like the RRSP meltdown strategy or help you see how your RRSP and TFSA balances compare to other Canadians at your age, because it can actually compare the alternatives.

4. Scenario testing

One plan is never enough. You need side-by-side comparisons, Monte Carlo stress-testing for market risk, and sensitivity analysis for inflation, longevity, and return assumptions. If you can't see your plan beside another plan, you can't make a real decision.

5. Updateable, not static

Life changes. Markets change. Tax rules change. A retirement plan that doesn't re-optimize when you update an input isn't a plan. It's a PDF. The whole point of software over a one-time advisor report is that the math stays current.

6. Plain-English explanations

Charts and numbers are not the same as understanding. The best tools explain why a recommendation makes sense for your specific situation, in plain language, grounded in your actual plan. AI is doing useful work here in 2026, but only when the explanations are tied to your inputs, not generic boilerplate.

7. Canadian data residency and PIPEDA compliance

Your retirement plan contains your net worth, your account balances, your medical assumptions, and your spouse's information. Where the data is stored matters. Look for Canadian data residency, PIPEDA (Personal Information Protection and Electronic Documents Act) compliance, and a clear privacy posture. If the company hosts everything on U.S. infrastructure with no Canadian footprint, factor that in.

8. Price you can actually live with

The right tool is one you'll actually keep using for 10, 15, or 20 years. That changes the math on pricing. A $5,000 one-time plan that goes stale in 18 months is more expensive than $249 a year of software that re-optimizes every time your inputs change. We'll do the actual math on this in a minute.

Common alternatives in the Canadian market

Here are the most common alternatives Canadians look at in 2026, in alphabetical order. Each is a legitimate option for the right type of user.

Adviice (adviice.ca)

A DIY Canadian retirement and tax planning tool founded by Owen Winkelmolen. The individual plan is $9/month or $49/year. It includes CPP and OAS projections, tax-efficient withdrawal scenarios, and AI-supported planning. Strong fit for Canadians who want a low-cost annual snapshot and are comfortable building scenarios themselves.

MoneyReady App (moneyreadyapp.ca)

Built by Elisabeth Tillier, a retired computational biologist. It combines personal-finance and retirement planning, with a "Time Machine" cash-flow engine, a CPP/QPP optimizer, a withdrawal strategy optimizer, and a Wealthica integration. Pricing is roughly $60 for the monthly trial, $160 for the first year, and $110 to renew. Best fit for hands-on DIY planners who want one tool covering both household budgeting and retirement modelling.

PlanEasy (planeasy.ca)

A fee-for-service planning firm rather than a pure software platform. PlanEasy offers interactive online sessions: Retirement Consult, Comprehensive Planning, and Ongoing Planning. You're paying for a planner's time, with software supporting the engagement. Best fit for Canadians who want a human in the loop and prefer scheduled review meetings over self-serve tooling.

Snap Projections (snapprojections.com)

Cloud-based Canadian financial planning software built for advisors, planners, and wealth managers, not direct-to-consumer. It runs side-by-side scenarios including CPP and OAS timing and corporate planning. Pricing is roughly $69/month, $828/year for Advisor Professional, and $1,188/year for Advisor Business. Best fit for advisors running plans for clients. Most retail Canadians won't be the direct buyer here.

The pricing reality check

Here's a number most Canadians don't realise. A detailed one-time retirement plan from a Canadian fee-only planner typically costs $3,000 to $5,000. Complex cases (incorporated business owners, U.S. exposure, expat planning) commonly run $5,000 to $10,000 or more.

Now run the math the other direction. Optiml Pro+ is $24.99/month, or $249 a year. Ten years of Pro+ comes out to roughly $2,500. That's the same total cost as a single one-time advisor plan. The difference is that the software plan re-optimizes every time your inputs change. The advisor PDF doesn't.

One thing worth saying before we get to the numbers. The cost column is only half the equation. What the software saves you matters just as much. For Optiml users, the illustrative impact on lifetime tax lands in the 3 to 15% range of total household tax paid, which on most Canadian retirement households is many multiples of the subscription cost over a 30-year horizon. Then add the stress reduction of having a plan you can rerun whenever your inputs change, the hours you don't spend trying to optimize this yourself in a spreadsheet, and the confidence of seeing every account, every year, in one connected picture.

With that context, here's how the Canadian options stack up on cost over a realistic 10-year horizon:

Annual ranges based on each provider's public pricing as of May 2026. Fee-only planner range based on Canadian fee-only firms (e.g., Objective Financial Partners) and MoneySense industry coverage.

You can see Optiml's pricing in full on the pricing page.

How Optiml stacks up against each criterion

Here's where Optiml lands on the same eight criteria, in order. No fluff.

- Canadian-rule accuracy: RRSP, RRIF, TFSA, FHSA, LIRA, and LIF supported across every province and federally. OAS recovery tax modelled at the 15% rate above the threshold on a prior-year-income basis. CPP early-take and deferral percentages, pension income splitting at 65, and GIS guardrails are all built in.

- Whole-household modelling: spouse-level accounts, pension splitting, survivor benefits, and joint assets are first-class. The Legacy plan also models CCPC structures, including HoldCo, OpCo, family trusts, and joint partner trusts.

- True optimization: Optiml simultaneously solves deposits and withdrawals across every account, every year, against your choice of objective (maximum after-tax estate, maximum lifetime spending, or minimum lifetime tax). The illustrative impact is a 3-15% improvement in after-tax estate at the same lifestyle. For a deeper look at one specific strategy, see why RRSP meltdown strategies are often overlooked.

- Scenario testing: Compare Plans lets you store and run up to 20 scenarios side-by-side. Success Score stress-tests your plan against 50 market scenarios drawn from 50,000+ generated return paths.

- Updateable: your plan lives in your account. Change an input and the optimization re-runs.

- Plain-English explanations: Eva is the in-platform AI assistant, grounded in your specific plan, available on Pro+ and Legacy.

- Canadian data residency and PIPEDA compliance: Canadian-hosted data, PIPEDA compliant, BBB A+ rated.

- Price: Optiml lite (free), Essentials ($9.99/mo), Pro+ ($24.99/mo, most popular), Legacy ($49.99/mo for incorporated Canadians).

For context on the platform itself, the proof points are factual: 140,000+ retirement plans run, 4.8/5 user rating, coverage in The Globe and Mail and the Financial Post, and a $25K Invest Nova Scotia grant. The full feature list is on the features page, and a walkthrough is on how Optiml works.

Why we built Optiml

The honest answer is that the math was inaccessible. Retirement-income optimization is well-studied in academic literature, but most Canadians had no practical way to access that math directly. You either paid $3,000+ for a one-time plan that aged out, paid a percentage of assets to someone with software that was opaque to you, or you tried to do it yourself in a spreadsheet you knew was wrong.

Optiml was built by Oltre Financial Inc. in Halifax, Nova Scotia, and launched in September 2024. The team is three founders: Zac Davies (CEO), Max Jessome (COO), and Alex Ingham (Co-Founder). The goal was simple. Take the optimization math that institutions have used for decades and put it in the hands of self-directed Canadians and the advisors who want better tools.

Questions to ask before picking any retirement planning software

Before you pay for anything, run any candidate through these six questions. If a tool can't answer all six confidently, keep looking.

- Does it model every Canadian account I actually have (FHSA, LIRA, spousal RRSP, RRIF, RDSP, RESP)?

- Does it handle my full household (spouse, real estate, and if applicable, my corporation)?

- Does it actually optimize, or does it just simulate a rule of thumb?

- Can I compare scenarios side-by-side and stress-test against bad markets?

- Will the plan stay current as my inputs change?

- Is my data stored in Canada, and what's the all-in cost over 10 years?

Frequently asked questions

What is the best retirement planning software in Canada?

It depends on whether you're planning yourself or with an advisor. For self-directed Canadians, Optiml is the most complete optimizer covering RRSP, TFSA, FHSA, LIRA, CPP, OAS, real estate, and corporate accounts. For advisor-led planning, Snap Projections is the most-used Canadian platform. For low-cost yearly snapshots, Adviice covers the basics at around $49/year.

How much does Canadian retirement planning software cost?

Self-serve software runs $50 to $500/year (Adviice, MoneyReady, Optiml). Advisor-grade platforms like Snap Projections run $800 to $1,200/year. A one-time fee-only advisor plan typically costs $3,000 to $5,000, with complex cases routinely exceeding $10,000.

Is Optiml better than a financial advisor?

Optiml is a planning and optimization platform, not a replacement for personalized human advice. Many Canadians use Optiml alongside their advisor, bringing the optimized plan into the meeting so advisor time goes to judgement rather than math. If you'd like a related read on this mindset, see how to stop feeling guilty and spend more in retirement.

Can I use retirement planning software if I have a corporation (CCPC)?

Yes. Optiml's Legacy plan ($49.99/mo) models HoldCo, OpCo, family trusts, joint partner trusts, CDA, GRIP, ERDTOH, NERDTOH, and salary-vs-dividend optimization. Most consumer planning tools don't model CCPC structures at all, which is the biggest gap in the market for Canadian business owners.

How is Optiml different from Adviice?

Both are legitimate Canadian planning platforms. Adviice focuses on scenario projections and runs around $49/year. Optiml runs mathematical optimization across deposits and withdrawals together, plus Success Score stress-testing, Eva AI explanations, Wealthica integration, and full corporate planning in Legacy. Different tools for different jobs.

Does Optiml work with my advisor?

Yes. Many Canadians bring an Optiml plan into their advisor meeting as a starting point. Pro+ and Legacy include CSV and XLSX export, formulas included, so your advisor can review the underlying math.

The Bottom Line

The best Canadian retirement planning software isn't just the one with the prettiest dashboard. It's the one that gets the Canadian rules right, models your full household, actually optimizes (rather than simulating a rule of thumb), updates when your life updates, and costs something you'll still be paying ten years from now without resenting it.

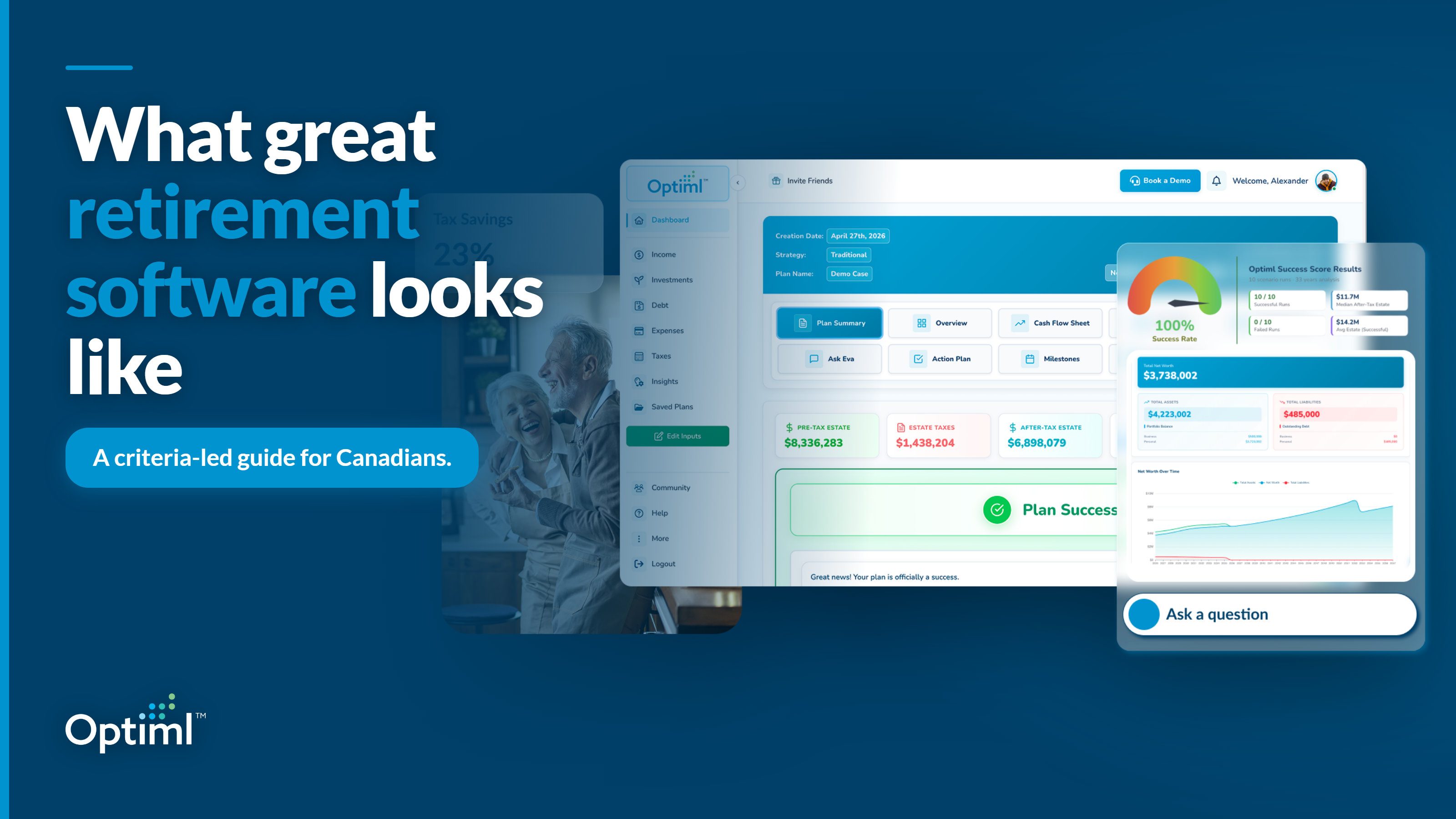

On the dashboard front specifically, we've heard from many Optiml users that the interface, the graphs, and the overall user experience are the cleanest and easiest they have tried in this category. That matters more than people think, because the right tool is the one you'll actually open every month, not the one that sits in your bookmarks gathering dust.

Run any tool through the eight criteria above and the six pre-purchase questions. The answer becomes obvious quickly.

It's not about finding the cheapest plan. It's about finding the one that keeps working for you.

Ready to optimize your retirement plan?

Join thousands of Canadians making smarter financial decisions with Optiml.

Start Free Trial