Retirement Withdrawal Planning, Year by Year. Built for Canadians.

The year-by-year plan that draws from Registered Retirement Savings Plans (RRSPs), Tax-Free Savings Accounts (TFSAs), Registered Retirement Income Funds (RRIFs), and Canada Pension Plan (CPP) and Old Age Security (OAS) in the order that protects your savings and your tax bill.

4.8 / 5 average rating · BBB A+ · 175,000+ retirement plans run · PIPEDA compliant — AES-256 encryption; AWS Canadian data center

Cancel anytime in-app.

As featured in the Globe and Mail

As featured in the Financial Post

BBB A+

PIPEDA compliant — AES-256 encryption; AWS Canadian data center

The decumulation problem

You spent 30 years building it. Now you need a plan to draw it down.

Most retirement advice is about accumulation: saving, investing, growing the pot. Decumulation is a different problem, and the rules are unforgiving. Withdraw in the wrong order and you may pay more tax than you need to. Withdraw too aggressively and you risk outliving your savings. The RRIF tax cliff at 71 catches Canadians who did not plan ahead. Optiml builds the year-by-year withdrawal plan across every account. RRSP Meltdown, RRIF conversion timing, TFSA top-ups, and CPP and OAS timing, all coordinated. You see the plan year by year, balance by balance, tax by tax.

Every drawdown decision in one plan

Every withdrawal-planning outcome Optiml models for you.

Retirement withdrawal strategies in Canada depend on your accounts, your timeline, and your partner's plan. Optiml coordinates every lever in one year-by-year model.

The optimal withdrawal order

Which account first? RRSP, TFSA, RRIF, non-registered, corporate? Optiml sequences withdrawals across every account, year by year, to minimize lifetime tax while keeping your plan resilient. Powered by the Withdrawal Optimizer.

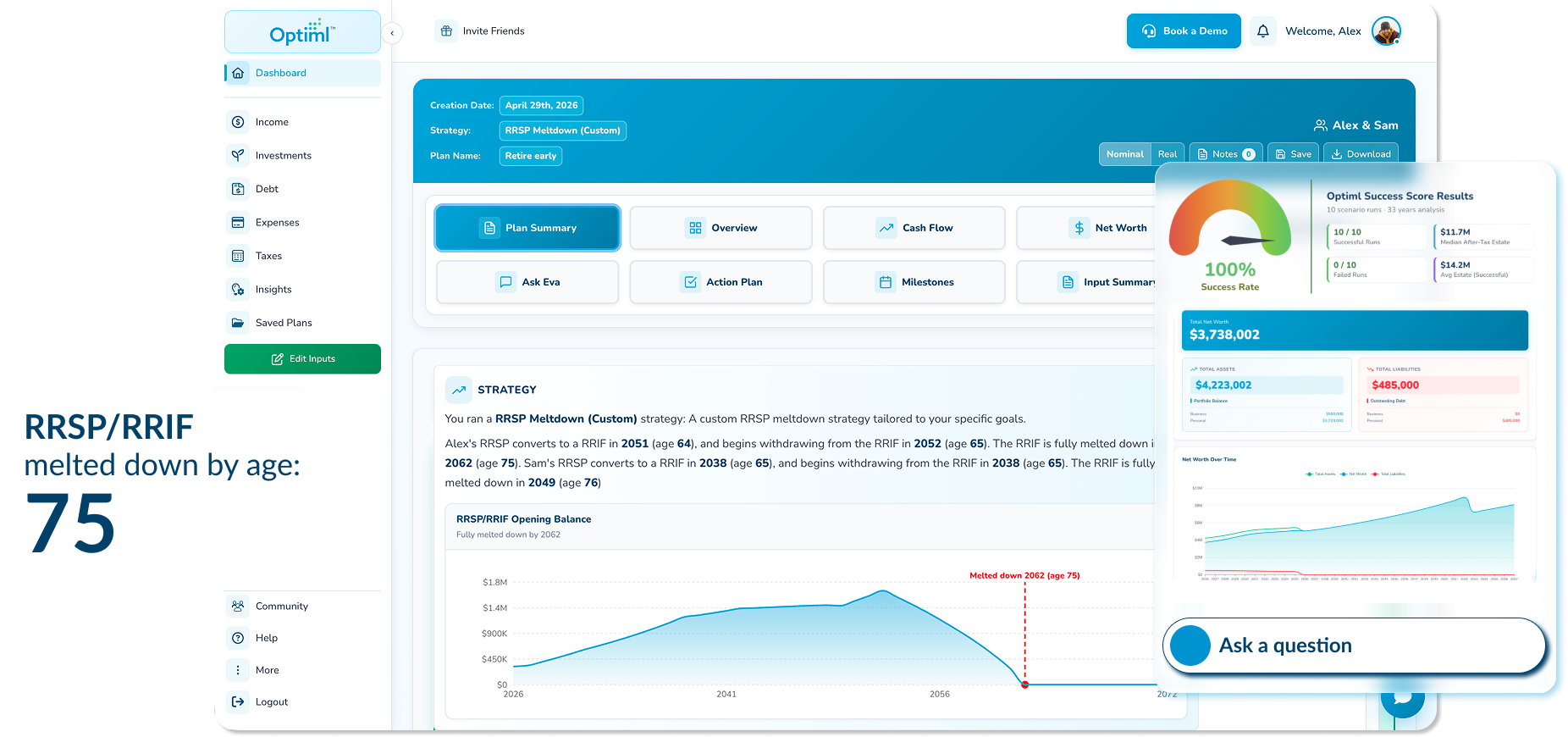

RRSP Meltdown, three approaches

Drawing down your RRSP before age 71 can flatten the RRIF tax cliff. Optiml models three approaches (conservative, moderate, aggressive) so you can see the trade-offs in tax, income, and what you leave behind. Powered by RRSP Meltdown.

RRIF conversion timing

You must convert your RRSP to a RRIF by 71, but you can start earlier. Optiml models the optimal age to convert based on your full income picture, including OAS clawback exposure. Powered by RRIF modelling.

CPP and OAS timing as a withdrawal lever

When to take CPP and OAS is not only about benefit amounts. It is a withdrawal-planning lever. Delaying CPP can let you draw more from your RRSP at a lower bracket. Optiml runs every combination. Powered by the CPP & OAS Optimizer.

Tested against bad years

Withdrawal plans that look fine in average markets can fail in bad ones. Optiml runs your plan through thousands of Monte Carlo paths and shows the odds of your money holding up. Single resilience score, 0 to 100. Powered by Success Score.

What you leave behind

Decumulation is not only about you. Optiml projects what is left at the end of your plan after every year of withdrawals, taxes, and growth, so you can see the trade-off between drawing more now and leaving more behind. Powered by Estate Projector.

Cancel anytime in-app.

How it works

Three steps. You stay in the driver's seat.

Get your first withdrawal plan up and running quickly, then add detail to fine-tune as you go. Re-run in seconds when life changes.

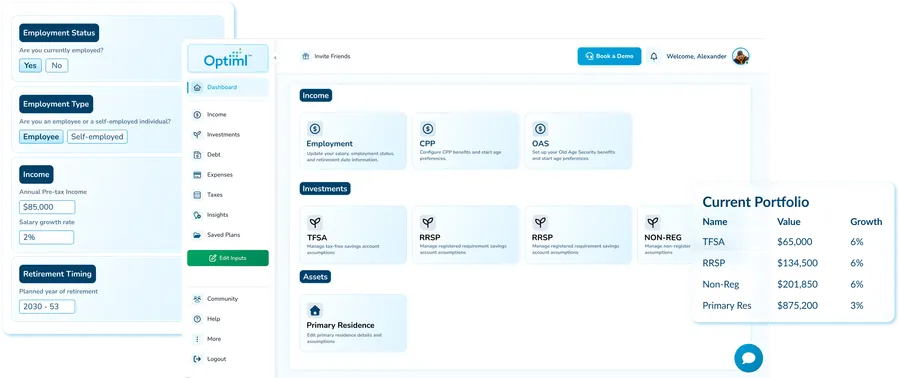

Input your full picture.

Accounts, real estate, pensions, CPP and OAS situation, your partner's plan, and lifestyle spend. Most Canadians get their first plan running in 15 to 45 minutes, depending on complexity. Start with the essentials and fine-tune with more detail anytime. Optional direct bank account linking on Pro+.

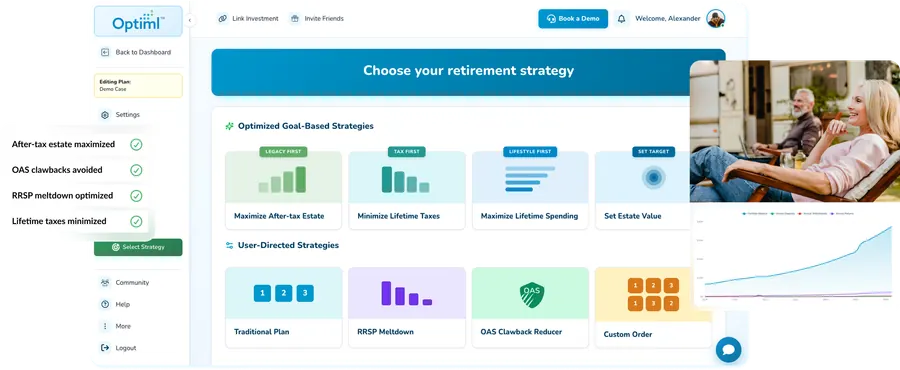

Pick your strategy. Optiml models every withdrawal year.

Choose what you want to optimize toward: increase after-tax estate, build a plan to spend it all, minimize lifetime tax, or fully customize your plan. Withdrawal order, amounts, taxes, balances, RRIF conversion, and CPP and OAS timing are all coordinated against Canadian rules.

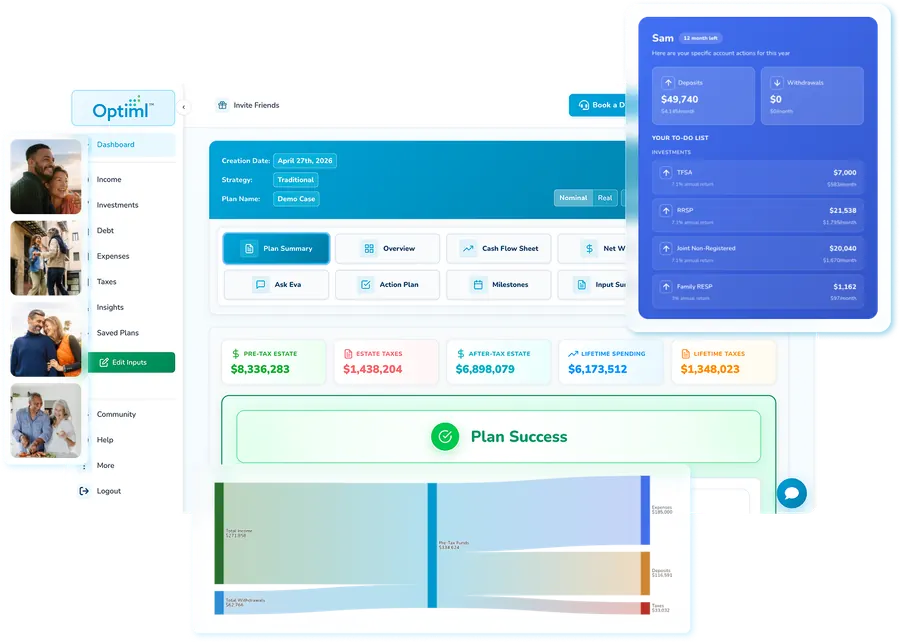

You drive the plan.

Adjust spend, test scenarios, and compare RRSP Meltdown approaches. Add more detail over time to fine-tune, then save the plan you want. Optiml then gives you your action plan, showing exactly how to achieve your goals.

Rule of thumb, advisor, or software

Three ways to plan retirement withdrawals. Pick the one that fits.

Most Canadians searching for retirement withdrawal strategies in Canada are choosing between a rule of thumb, a financial advisor, and software like Optiml.

| Feature | A rule of thumb | A financial advisor | |

|---|---|---|---|

| Cost | $249/year (most popular plan) | Free, but generic | $3,000 to $5,000 a year (about 1% of assets) |

| Withdrawal order | Optimized for your plan | "4% rule" or similar | Their model, often opaque |

| RRSP Meltdown | Three approaches, modelled | Not modelled | Sometimes discussed |

| RRIF timing | Optimal for your tax picture | Default = age 71 | Default = age 71 |

| Stress-tested for bad years | Yes, Monte Carlo | No | Sometimes |

| Plan visible year by year | Always | No | Sometimes |

| Who drives the plan | You | You | Them |

| Updates | Always current | Stale | Annual |

Real Stories from Real Canadians

Thousands of Canadians are already using Optiml to take control of their retirement. Here is what they have to say.

"

"I love this software. It is so easy to use, and so intuitive. The scenarios and stress testing functions are great to give yourself a sense check. On top of this, the help desk is super responsive and seems to really care about what they do. Highly recommend."

JW

JMW

Google Review

1 / 33

"

"I love this software. It is so easy to use, and so intuitive. The scenarios and stress testing functions are great to give yourself a sense check. On top of this, the help desk is super responsive and seems to really care about what they do. Highly recommend."

JW

JMW

Google Review

"

"Optiml has been incredibly useful, easy to use, full of insights and time saving (I used to try to do my own models on spreadsheets!). The truth is, I am not sure why everyone is not using this tool for their financial and retirement planning, and I recommend the platform anytime discussions on financial retirement planning come about."

AM

Ale MC

Google Review

"

"The real people customer support and technical teams at Optiml are fantastic, actually, second-to none! They respond quickly and accurately to help you work through any issues. EVA is really great also; she provides excellent details and helps with almost everything (and trust me, I ask a lot of questions!); if you're stuck though, or something doesn't make sense, the real people at Optiml are there to back her up within hours, not days."

KM

Karen Marshall

Google Review

"

"Best DIY retirement planning software and absolutely incredible support for any questions."

ED

Elias Daskalakis

Google Review

"

"I've been using Optiml Pro+ for DIY planning for almost a year now. I found the platform easy to navigate, and when I did have some questions they were very responsive and helpful. It is easy to test and compare various assumptions. They are continuously improving the platform with upgrades such as the cash wedge and scenario management features. Highly recommended."

SH

Stephen Hamada

Google Review

"

"Great piece of code / platform. Go blow the doors off the establishment!"

DH

Derek Hulbig

Google Review

Page 1 of 6

What Optiml Actually Gives You

Not features. Outcomes.

Behind every tool is a feeling. Confidence. Clarity. Control. Here is what Optiml is really built to give you.

Yes, you can retire.

Stop wondering if you have enough. Optiml runs your complete financial picture and gives you a clear, honest answer backed by math, not guesswork.

Built to carry you forward.

Your plan is stress-tested across market downturns, rising inflation, and varying returns. See the odds your income holds up, year by year, modelled against thousands of market paths.

More for your family.

Optiml models the most tax efficient way to pass on your estate. Avoid unnecessary tax liabilities so your beneficiaries keep what you worked hard to build.

Your plan, on your terms.

Update your financial plan from home. No calls, no emails, no waiting. Make a change and see the impact in seconds. You are in control, always.

Know exactly what to draw, and when.

Get a year by year withdrawal roadmap showing which account, how much, and in what order. No spreadsheets. No guessing. Just a clear path through retirement.

See your tax picture, start to finish.

Watch how your tax liability evolves through every stage of retirement. Identify the windows where smart moves make the biggest difference.

Frequently asked about retirement withdrawals

Questions Canadians ask before planning their drawdown.

Simple Canadian pricing

Pick a plan and start your 14-day free trial.

All plans are in Canadian dollars. Every plan includes a 14-day free trial, and you can cancel anytime in-app.

Monthly

Annual

Save up to 20%Essentials

Peace of mind, simplified.

$99

/yr

Save 20%

✓

Retirement calculator

✓

Tax-optimized strategies

✓

Eva: Your AI assistant

✓

Deposit & withdrawal strategy

✓

Estate planning

Pro+

Most popular for serious planners.

$249

/yr

Save 20%

✓

Everything in Essentials

✓

CPP / OAS optimizer

✓

Success score

✓

Compare plans

✓

Save & store 20 plans

✓

Download plans

Legacy

Built for business owners.

$499

/yr

Save 20%

✓

Everything in Pro+

✓

Trust planning

✓

Holding Company (HoldCo)

✓

Operating Company (OpCo)

✦ Every plan includes a 14-day free trial

View full feature comparison →

Built in Canada

“We built Optiml to empower Canadians to build their own financial plans and gain the confidence to make informed decisions about their financial future.”

Zac Davies

Co-Founder & CEO, Optiml

Headquartered in Halifax, Nova Scotia

See the year-by-year withdrawal plan. Built around your accounts, your taxes, your timeline.

4.8 / 5 average rating. 175,000+ retirement plans run. 14-day free trial on every plan.

Cancel anytime in-app.

Cancel anytime in-app.